Ever wondered why people lease cars? It may seem like a waste of money to a lot of people. However, that’s not always true, and your individual circumstances can change the calculation of whether to purchase or lease. Let’s dive into this decision-making process.

Let’s get some upfront things out of the way:

- For the same MSRP (sticker price), a monthly payment on a lease will be less than a purchase (finance).

- With leasing, the owner does not actually own the car. The car is leased to the offer, usually by the manufacturer, with the lessor taking back ownership at the end of the lease term, unless the owner decides to purchase the car, which is a separate transaction.

- Lease agreement lengths are usually between 24 months and 36 months.

- There is no bank or lender that is lending money for a payment, like in the case of financing a purchase. Thus, there is no interest rate or APR, but there is something similar to interest, called Money Factor, which is essentially an additional cost of leasing.

- Leasing almost always applies to new cars at the time of the lease start. There are exceptions to this, particularly lease swaps, which are when a lessee transfers their lease agreement to another individual, although the new individual will need to be approved by the lessor, and not all brands allow this.

With this in mind, let’s examine a scenario where leasing would be more costly than purchasing.

Here’s the terms for a finance purchase for a 2024 Honda Accord EX:

MSRP

Tax and Title in Los Angeles, CA

Total Purchase Price (out the door)

Finance Term

Down Payment

Total Loan Amount

Interest Rate

Total Interest Amount

Total of 60 Payments, with Interest

Monthly Payment

$31,005

$3,404

$34,409

60 months (5 years)

($5,000)

$29,409

8%

$6,369.50

$35,778.50

$596.31

Now, let’s examine this same car as a lease agreement:

MSRP

Tax and Title (only for lease term)

Acquisition Fee

Total Purchase Price (out the door)

Lease Term

Down Payment (capitalized cost reduction)

Money Factor

Total of 36 Payments

Monthly Payment

$31,005

$2,249

$595

$33,849

36 months (3 years)

($5,000)

0.00213, equivalent to 5.11% APR

$13,680

$380

Let’s see that for both scenarios, the buyer wants to have the car for 8 years. With the lease, the buyer will have to continue to lease after the original 36 lease term ends. Let’s assume that they lease the same car model for the same amount over 8 years.

The finance purchase will have the buyer finishing payments by 5 years, with 3 years of no payments. The lessee will have 8 years of continuous payments, albeit at a lower amount. After 8 years, the total payments will amount to $36,480, which is more than the total finance payments of $35,778.50.

However, the lessee will have gotten 3 new cars over this 8 year term, while the finance buyer would only have 1 new car. Still, the finance buyer also has equity in their purchase, as they are the owner. After 8 years, the Honda Accord has a predicted residual value of 32%, or $9,580 in value. This is value that a lessee would not have.

But, how can leasing ever make financial sense, then?

Even things that make the most financial sense aren’t always followed in reality. Everyone spends beyond their absolute minimum, to varying degrees. The calculation probably would still make financial sense if the buyers held their cars for 5-6 years. Additionally, vehicles with high resale value, like the Honda Accord, are usually better to purchase. These vehicles also tend to be quite reliable, so holding on to them for years after finishing your finance term makes them solid options.

But, there are many people who purchase a car right around when their finance term ends, or even before it ends, by trading it in. If you’re someone who has almost always had a car monthly payment, leasing is likely better for you, depending on the market and car model you buy.

Leasing is different than purchasing in that the manufacturer (lessor) can set the monthly payment amount that is not directly tied to the purchase price or MSRP. What I mean by this, is that because there is no lender and total amount financed, it’s almost like renting a car. The value of the car still factors into the lease payment amount, but the residual value of the car factors into the actual lease payment amount, and manufacturers can set much more favorable payment amounts compared to financing.

We saw above that the 2024 Honda Accord had an Out the Door lease payment of $380, a finance payment of $596, with an MSRP of $31,005.

Let’s see a car which has much more favorable lease terms, which these days, include a lot of EVs:

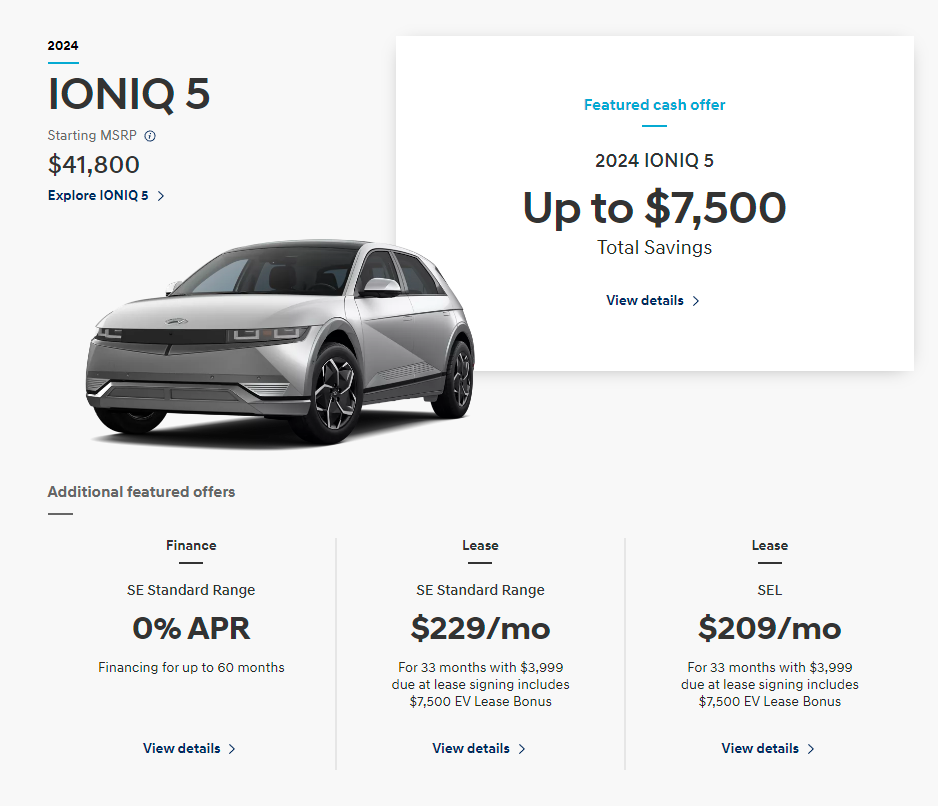

This IONIQ 5 is offering a lease of $209 a month. After tax and fees (which in leases, beware of drive-off or acquisition fees, which aren’t always clearly shown in ads and promotional material), this will be about $250/month, with $4,000 down. Financing this same car over 60 months, with the same amount down, would be around $600/month.

How does this IONIQ 5, with a higher MSRP, have a lower lease payment than the Honda Accord above?

This is where the manufacturer setting deals comes in. There are also deals on finance purchases, and these are usually a little more easier to understand, as they can be presented in terms of cash off the MSRP price, or an incentive. In leasing, it’s harder to decipher, but you can compare lease deals among manufacturers with their MSRPs and finance payment estimates to get a good idea.

Additionally, the $209/month lease is actually for the SEL trim model, which has an MSRP of $49,795, or $42,295 after EV incentive. That’s over $10,000 more than the Honda Accord.

The Honda Accord could have lease deals as well, which as of the time of this writing, looks to be in the $280/month range. Still, that’s higher than the IONIQ 5. After the EV rebate ($7,500) that all manufacturers are offering, by way of government incentives, these cars don’t have as big of an MSRP delta as may be presumed. But, the IONIQ 5 is still the more expensive car by about $12,000, and will still have a slightly lower lease amount.

Another example, using a car that has about the same MSRP as the IONIQ 5:

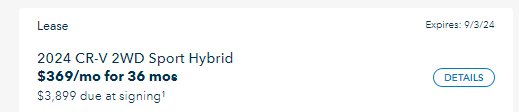

This CR-V Hybrid has an MSRP of about $35,700, compared to $35,695 for the IONIQ 5 SE, both after destination and government EV incentive, but without tax and title.

Both deals assume about $4,000 in down payment, yet the CR-V’s lease deal is at $369 compared to the IONIQ 5’s $209. That’s a HUGE difference.

Extrapolating this over 72 months, or 6 years, the leasee would pay about $26,000 total, including 2 down payments of $4,000 each. A finance purchase at 5% APR, which on the very low end, say with an amazing dealer discount, for this CR-V would be about $550 a month, with a total liability amount (after deducting equity) of $26,500, including one down payment of $4,000.

Basically the same, but the leasee enjoyed both lower payments and having a newer car for the entire 6 year period.

The bottom line?

Look for monthly lease deals on manufacturer websites, usually under “Special Offers”. There are some good deals out there, especially for models that manufacturers have a surplus of supply for. It may be wiser to lease that car instead of purchase it, particularly if your financial situation calls for lower monthly payments.

The catch is that you won’t enjoy equity at the end of the term, although we see that it still may not tip the scales in the favor of financing that much, if at all.

The other BIG catch is that, if you’re actually going to hold on to a car for a LONGER period, you should balance it more in the favor of financing. While it may seem obvious, the longer you hold onto a car that is paid off, the bigger your savings will be. But, we all know that some of us value having newer vehicles, in which case leasing may not actually be the waste of money that it can be portrayed as.

On top of all of this, there are mileage limits on lease deals, which are set for each deal, but are typically between 10,000 and 15,000 miles a year. The more miles allowed, the higher the payment. These lease deals shown above offer a standard 10,000 miles a year, after which you will pay for each mile above that, when you turn in the lease. If you drive more than this amount, leasing may not be for you.

You could purchase a car while leasing it to avoid the mileage limit, but this usually only makes sense if you’re in a unique situation where you need lower monthly payments at the start.

There are also other lease tricks, like one-pays and security deposits that can lower your payment further. In general though, vehicles like Hondas and Toyotas make more sense to finance, and used may be better than new.

For vehicles like entry-level luxury sedans, EVs, odd sportscars, and certain base SUVs, leasing may not be such a bad financial idea. After all, a lot of people aren’t driving the MOST financially prudent vehicles.

One response to “When to Lease a Car”

Hi, this is a comment.

To get started with moderating, editing, and deleting comments, please visit the Comments screen in the dashboard.

Commenter avatars come from Gravatar.